Crypto & U.S. Taxes Primer

First article in a series of articles about crypto taxes: Understanding crypto tax implications is critical whether an experienced crypto trader or gift receiver

The Relationship Between Crypto & Tax

Understanding cryptocurrency tax implications is critical whether you are an experienced crypto trader or received a small amount of crypto as a gift. One aspect of cryptocurrency investing that few discuss is the tax implications. Taxes are not the most exciting topic to discuss, and many people have no idea what they're doing.

People may refer to crypto as a digital currency, but in the eyes of most governments, it is not an actual currency. In Notice 2014-21, the IRS labels cryptocurrency as property. As a result, market participants must report capital gains and losses on Schedule D and, if applicable, Form 8949.

According to Baker Botts tax partner, Jon D. Feldhammer, cryptocurrency is treated as property and taxed accordingly. You'll have to pay taxes if you sell your crypto or NFT or trade them for another investment or purchase. If you buy one Bitcoin for $30,000 and then sell it for $50,000 a few months later, Feldhammer estimates that you would have $20,000 in short-term taxable gains. But even so, he mentions that things get complicated from here because it's common for people to make frequent trades for various reasons.

Assume someone has $50,000 in BTC and wishes to purchase an NFT. In that case, they may require Ethereum to buy a specific NFT, so they exchange BTC for ETH to complete the transaction. Feldhammer claims that you still have $20,000 in taxable income in this case because you exchanged the property (BTC) for another property (ETH), which is a taxable transaction.

How is cryptocurrency taxed?

You face capital gains or losses if you buy, sell, or exchange cryptocurrency in a non-retirement account. Like other investments taxed by the IRS, your profit or loss may be short-term or long-term, depending on how long you hold the cryptocurrency before selling or exchanging it.

Suppose you owned the cryptocurrency for a year or less before spending or selling it. Any profits are usually considered short-term capital gains and taxed at your ordinary income rate. If you hold the cryptocurrency for more than a year, profits are generally treated as long-term capital gains and taxed at long-term capital gains rates.

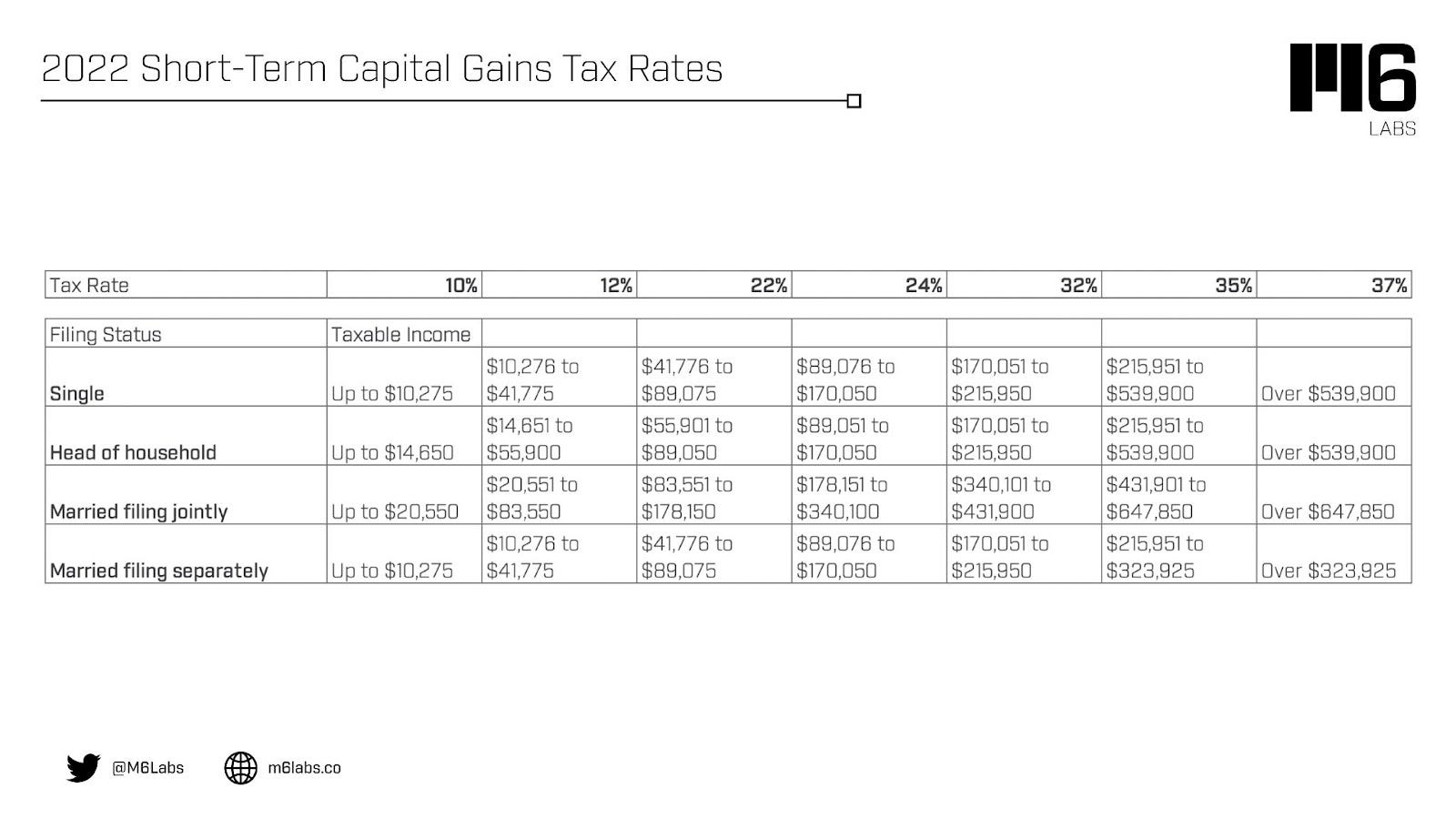

For short-term capital gains or ordinary income earned through crypto activities, you should use the following table to calculate your capital gains taxes:

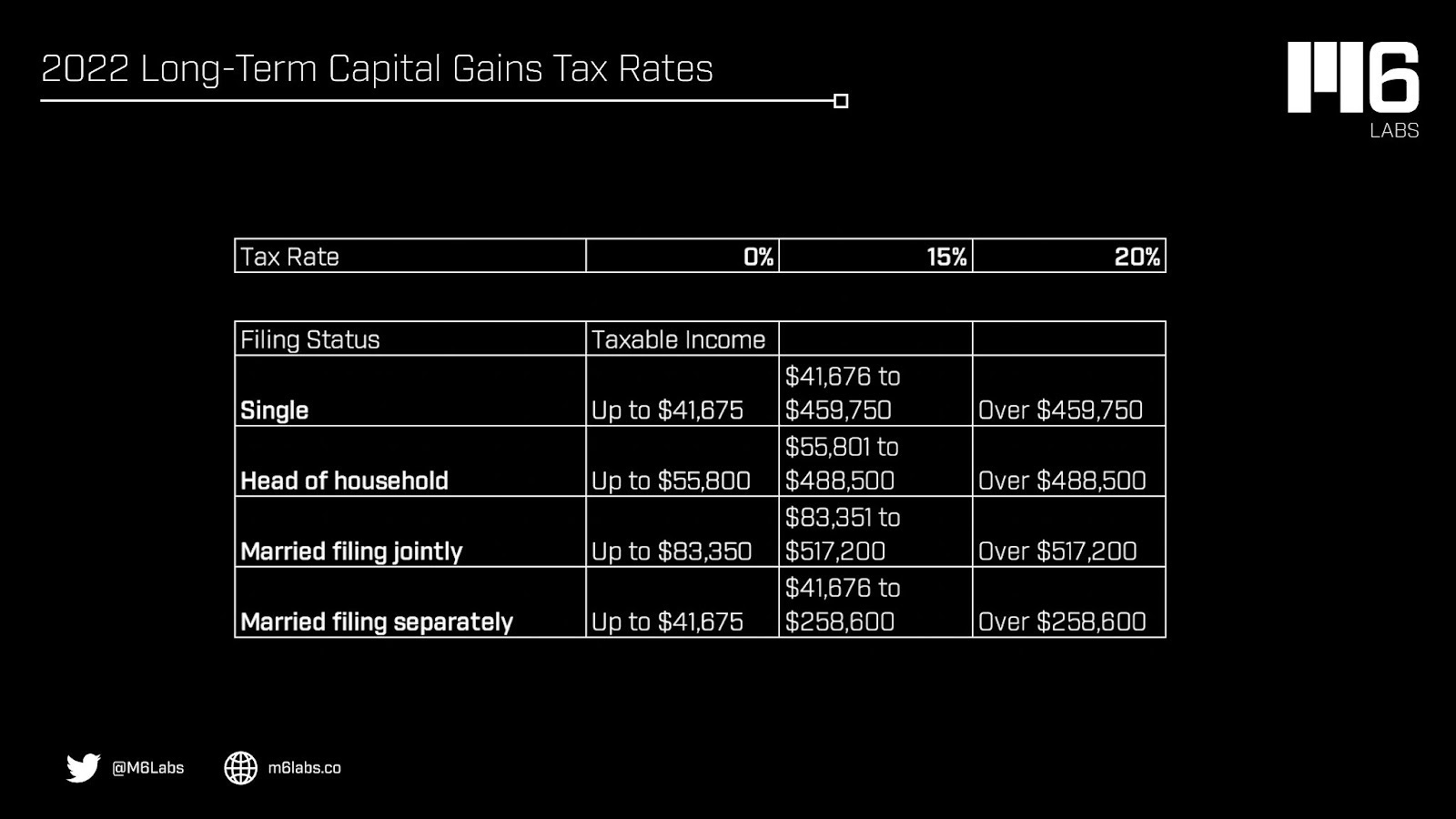

If you have held your cryptocurrency for more than one year, use the following table to calculate your long-term capital gains:

IRS guidance on the taxation of virtual currency

A virtual currency is defined broadly as a digital representation of value that serves as a medium of exchange, a unit of account, and a store of value. A convertible virtual currency is a virtual currency that has an equivalent value in real money or acts as a substitute for real money.

As the cryptocurrency landscape evolves, the IRS issued Rev. Rul. 2019-24 and a list of frequently asked questions about virtual currency transactions. Rev. Rul. 2019-24 addresses two unique scenarios: one in which a hard fork occurs. No new cryptocurrency is received by the taxpayer, and another in which a hard fork occurs, but the taxpayer gets units of a new cryptocurrency due to an airdrop.

When is your crypto taxable?

To determine whether you owe taxes, consider how you used your cryptocurrency.

Not taxable examples:

Purchasing cryptocurrency with cash and storing it - buying and holding cryptocurrency is not taxable. The tax is often incurred when you sell, and the gains are realized.

Donating cryptocurrency to a tax-exempt charity or non-profit - you donate cryptocurrency directly to a charitable organization such as GiveCrypto.org.

Getting a gift - if you get crypto as a gift, you won't have to pay taxes on it until you sell it or engage in another taxable activity like staking.

Giving a gift - you can give up to $15,000 per recipient per year tax-free (and higher amounts to spouses). If the value of your gift exceeds $15,000 per recipient, you must file a gift tax return (which generally does not result in any current tax liability). If you transfer cryptocurrency to someone else without purchasing goods or services, it may be considered a gift, even if you didn't intend it to be.

Transferring cryptocurrency to oneself - transferring cryptocurrency between wallets or accounts is not taxable. You can carry over your original cost basis and acquisition date to continue tracking your potential tax impact when you sell.

Taxable as capital gains:

Selling crypto for cash - if you sell your assets for more than you paid, you will owe taxes. You may deduct a loss from your taxes if you sell at a loss.

Converting one crypto to another - for example, if you use bitcoin to buy ether, you must technically sell your bitcoin before purchasing the new asset. The IRS considers this to be taxable because it is a sale. You'd owe taxes if you sold your bitcoin for more than you paid.

Spending cryptocurrency on goods and services - for example, if you use bitcoin to buy a pizza, you'll almost certainly owe taxes on the transaction. To the IRS, spending cryptocurrency is no different than selling it.

Taxable as income:

Getting paid in crypto

Getting crypto in exchange for goods or services

Mining crypto

Earning staking rewards

Earning other income

Getting crypto from a hard fork

Receiving an airdrop - as part of a marketing campaign or giveaway, you may receive an airdrop from a cryptocurrency project. Receiving an airdrop is considered income, and you must report the amount on your taxes. Check out the most recent IRS guidance on airdrops.

Receiving other incentives or rewards - this list is not exhaustive; there are numerous reasons you could receive free cryptocurrency. These can include learning tips or incentives such as receiving $5 in bitcoin for referring a friend to a cryptocurrency exchange. In any case, you must report these as income.

If you've made a lot of money from crypto, it may impact your tax bracket, and you may pay a higher tax rate on all of your earnings. You may visit IRS.gov for the latest guidance on federal income taxes.

The IRS issued over 10,000 tax notices to potentially noncompliant taxpayers in 2019. It sent out another batch of tax notices to suspicious taxpayers in mid-2020. No letters were sent in 2021, likely due to the IRS transitioning to remote work and addressing stimulus-related issues.

Additionally, with the passage of the Inflation Reduction Act in August, IRS audit efforts are expected to increase. The act appropriated $45 billion for enforcement activities, including digital asset monitoring and compliance activities. Over the next decade, the agency will invest these funds in auditing and tax collection tools and personnel.

In light of these developments, taxpayers dealing with cryptocurrency may be concerned about their exposure to IRS audits. Knowing the ins and outs of IRS audits and how to avoid them may remedy some fears.

According to the IRS, only a tiny percentage of people who bought, sold, or traded cryptocurrencies correctly reported those transactions on their tax returns. For the first time since 2014, the agency issued additional guidance on how cryptocurrency should be reported and taxed in October 2019.

Beginning with the 2020 tax year, the IRS changed Form 1040 to include the question: Did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency at any time during 2022?

If you check "yes," the IRS will likely expect to see income from cryptocurrency transactions on your tax return.

Crypto tax software allows you to keep track of all of these transactions, ensuring that you have a complete list of activities to report when it comes time to file your taxes. The software integrates with several virtual currency brokers, digital wallets, and other crypto platforms to import cryptocurrency transactions into your online tax software. This can include cryptocurrency trades and transactions involving virtual currency as a form of payment for goods and services.

Based on the crypto tax software, transaction reporting may resemble documentation you would file with your tax return on Form 8949, Sales and Other Dispositions of Capital Assets. The IRS may format it so they can easily import it into tax preparation software.

Can the IRS monitor cryptocurrency activity?

Despite the anonymity of cryptocurrencies, the IRS may be able to track your crypto activity. For example, if you trade on a cryptocurrency exchange that offers reporting via Form 1099-B, Proceeds from Broker and Barter Exchange Transactions, they will report your trades to the IRS.

Furthermore, the IRS employs blockchain analytics tools to identify the crypto activity of digital wallets and link it to individuals in cases where tax evasion or money laundering is suspected. As a result, you should ensure that you report all crypto activities on your tax return during the year.

Are you facing a crypto tax nightmare?

Jackson Hewitt Chief Tax Information Officer Mark Steber says that if taxpayers cannot pay by the Tax Day deadline, they can set up a payment plan with the IRS. Telling the IRS you didn't realize your cryptocurrency transactions were taxed isn't enough. According to Thomas Shea, Tax Partner at EY, if you've triggered a taxable exchange but lack the fiat to cover the tax, you can exchange additional assets for fiat, essentially a sell-to-cover.

If you're even slightly concerned about mucking up your crypto tax bill, you're better off consulting a tax professional. Walker claims numerous deductions are available for capital gains liabilities, and taxpayers can use multiple tax credits and deductions to reduce the income taxes owed.

Finally, here are a few practical ways to reduce crypto taxes:

Hold profitable cryptocurrency investments for at least a year before selling or using them. Long-term gains are taxed at lower rates than short-term gains.

Make use of tax loss harvesting. If you've made profits and losses on various types of cryptocurrency, you can sell both and use the losers to offset your earnings.

Consider establishing a crypto IRA. This type of account, like other IRAs, allows you to make tax-deductible contributions and only pay taxes when you withdraw funds.

Crypto natives who want to play by the rules, or at least the few existing rules, have a few options. They can manually calculate their crypto taxes, hoping to pay the correct amount. Or they can use tools that reduce their tax burdens and allow them to keep more cryptocurrency after taxes.

There is more to say on this subject, and it is crucial to keep people informed about it. Stay tuned for future content surrounding crypto taxes!

Subscribe to receive our daily brief, extended weekly newsletter, and in-house research content!

Please Share, Leave Feedback, and Follow Us on Twitter, Telegram, and LinkedIn to stay connected with us.